Is the Transpacific Shipping Bubble About to Burst? 2025 Contract Rate Outlook

Written on August 17, 2025

by Adrian Stan

In the following categories: Container Shipping Industry, News, Shipping Container Sales

The 2025 transpacific shipping market is shaping up to be one of cautious optimism mixed with underlying instability. As analysts evaluate contract settlements for the May 2024 – April 2025 period, it’s clear that the container shipping industry is entering a delicate phase. Rates are rising modestly, but carriers continue to face overcapacity and stiff competition. Could this signal the start of a market correction—or the stabilization shippers have been waiting for?

Rates Are Up—But Not By Much

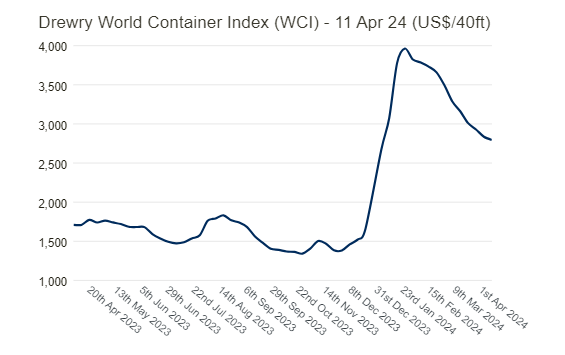

According to Jefferies, Asia–U.S. West Coast contract rates have settled between $1,400 and $1,500 per FEU—a slight uptick from last year’s $1,200–$1,300 range. However, these contract rates remain far below current spot prices, which are hovering around $3,000 per FEU. This gap underscores how spot markets continue to reflect volatility, while long-term contracts signal a cautious return to pre-pandemic norms.

In essence, carriers have not been able to translate strong spot performance into robust contract gains—an indicator of limited pricing power in an oversupplied market. Analysts suggest that the current equilibrium may not last, particularly if global freight demand softens later in 2025.

Tiered Contracts and Power Imbalance

Linerlytica reports a growing trend of tiered contract structures. Larger beneficial cargo owners (BCOs) are locking in rates below $1,400 per FEU, while smaller shippers remain in the $1,400–$1,500 range. This tiering reveals a fragmented market where carriers are willing to cut deals with big players to secure long-term volume commitments.

For smaller BCOs, the challenge lies in negotiating competitive terms amidst carrier competition and excess vessel supply. As newbuild deliveries from Asian shipyards continue to flood the market, capacity imbalances are expected to persist through 2025, making rate increases harder to sustain.

Spot vs. Contract Rates: Back to 2019?

Contracted freight rates are now roughly equivalent to pre-pandemic 2019 spot prices. While this normalization suggests market maturity, it also highlights the difficulty carriers face in maintaining profitability after years of historic highs. Carriers like Maersk and MSC, who benefited from the 2021–2023 boom, are now focusing on operational efficiency and digitalization to offset reduced margins.

As Sea-Intelligence notes, pricing volatility continues to challenge both shippers and liners. Their analysis emphasizes how “capacity chaos”—caused by rerouting, blank sailings, and geopolitical disruptions—creates downward pressure on rates even when demand remains solid.

U.S. Import Demand Remains Strong

Despite lower long-term contract rates, U.S. import volumes remain resilient. Data from Descartes shows March 2025 imports reached over 2.1 million TEUs—a 21% increase compared to pre-pandemic March 2019. Strong retail restocking, e-commerce growth, and strategic inventory management are fueling this momentum, particularly on West Coast gateways like Los Angeles and Long Beach.

Still, higher volumes do not always mean higher profits. With intense competition and mounting operating costs, carriers are struggling to maintain profitability despite increased trade activity.

Capacity Chaos and Pricing Volatility

The industry’s biggest challenge in 2025 remains balancing supply and demand. Continuous new vessel deliveries—especially megaships from Asian builders—are outpacing scrappage rates, keeping global capacity high. This imbalance has weakened carriers’ negotiating leverage and made rate increases unsustainable without significant demand growth.

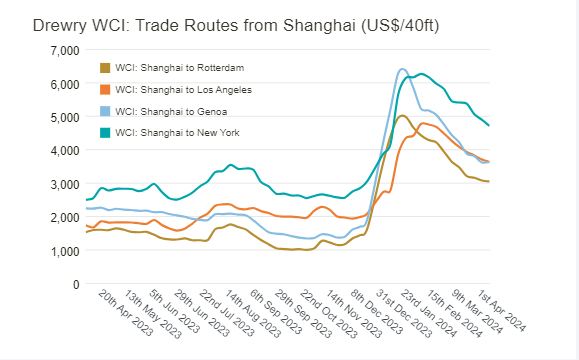

In parallel, geopolitical instability, including conflicts affecting the Red Sea and Suez Canal shipping lanes, adds complexity to routing and scheduling, further affecting reliability and costs.

The Bottom Line

The transpacific shipping contracts for 2024–2025 point to a market cooling from the record highs of 2023. While rates have inched upward, overcapacity and buyer leverage continue to restrict carrier profitability. The big question: will spot rates eventually align with contract levels—or could renewed global disruptions trigger another surge?

One thing is clear: 2025 will be a pivotal year for freight pricing strategy. Shippers should stay informed, leverage flexible contracts, and track developments across major trade routes.

Related Resources

- Global Shipping Heats Up: Spot Rates Surge as Demand Outpaces Capacity

- Global Shipping Trends 2024: Resilience Amidst Geopolitical Shifts

- The Impact of Houthi Attacks on Red Sea Shipping and the Suez Canal

- The Current Market for Empty Shipping Containers in the United States

- 2025 Shipping Container Trends: Industry Guide

For updates on container market dynamics and pricing insights, visit YES Containers or Get a Quote to check 2025 shipping container prices in your region.